Cost of Goods Manufactured COGM How to Calculate COGM

Cost of Goods Manufactured COGM How to Calculate COGM

March 11, 2020 Comments Off on Cost of Goods Manufactured COGM How to Calculate COGMContent

Thus, the total cost of goods manufactured for the period would be $265,000 ($100,000 + $50,000 + $125,000 + $65,000 – $75,000). This means that Steelcase was able to finish $265,000 worth of furniture during the period and move this merchandise from the work in process account to the finished goods account by the end of the period. Finished goods are valued by taking your starting inventory, adding your cost of goods purchased or manufactured, and subtracting the cost of goods sold. Here’s what finished goods inventory is, how to calculate it, and why it’s one of the best types of inventory out there. Lower COGS means higher profitability, and that you’ll likely pay more taxes. But the company made more money and we have a more valuable business!

What is cost of goods sold statement?

What is a Cost of Goods Sold Statement? A cost of goods sold statement compiles the cost of goods sold for an accounting period in greater detail than is found on a typical income statement. This statement is not considered to be one of the main elements of the financial statements, and so is rarely found in practice.

This impact is reflected through adjustment of inventories of finished goods. Allocated production overheads such as power, factory rent and machinery depreciation etc. Direct wages such as salary of factory workers, shop floor supervisors, quality check workers who are dedicated to the production process. And are in force, then it may also help them in fixing the amount of production along with profit-sharing bonuses. Once all of this is ready, it’s time to put together a complete schedule of Cost of Goods Manufactured and Cost of Goods Sold. Then, the value for the Cost of Goods Manufactured is transferred to the account for the final inventory named the Finished Goods Inventory account, where it is used to compute the Cost of Goods Sold. Usually, timesheets and time logs are used, and the business takes the total number of hours the employees worked and multiplies these by the hourly wage rate.

Definition of Cost of goods manufactured or COGM

Cost of goods sold is the cost of producing the goods sold by a company. It includes the cost of materials and labor directly related to that good. However, it excludes indirect expenses such as distribution and sales force costs. As a company selling products, you need to know the costs of creating those products. That’s where the cost of goods sold formula comes in. Beyond calculating the costs to produce a good, the COGS formula can also unveil profits for an accounting period, if price changes are necessary, or whether you need to cut down on production costs.

It is a critical duty to maintain a labor force that can meet expected production. John Manufacturing Company, a manufacturer of soda bottles, had the following inventory balances at the beginning and end of 2018.

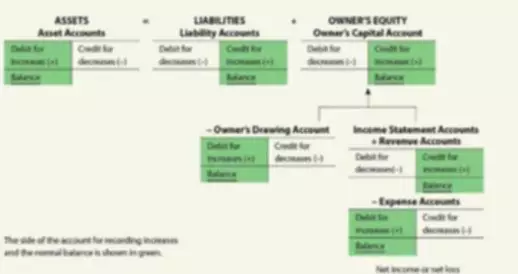

Management Accounting

Next, determine the beginning and ending inventories. Calculate the value of the inventory at the start and finish. Cost of goods sold is $200,000, the beginning balance in Finished Goods is $50,000, the ending balance in Finished Goods is $100,000, and the ending balance of Work in Process is $10,000. In a job order cost system, a credit to Manufacturing Overhead will be accompanied by debit to A.

For example, to make one gallon of chocolate milk, you need 0.950 gallons of whole milk and 0.05 gallons of chocolate syrup. Direct materials, direct labor, and overhead all get input into the production process. Therefore, to compute the cost of goods manufactured, think about all product costs, including not only direct materials but also direct labor and overhead. The cost of goods manufactured https://www.bookstime.com/ is the cost assigned to produced units in an accounting period. The concept is useful for examining the cost structure of a company’s production operations. The best approach to examining the cost of goods manufactured is to disaggregate it into its component parts and examine them on a trend line. Glue, gloves, foil, tape, fittings and fasteners are a few examples of indirect materials.

Manufacturing overhead includes

If the inventory value included in COGS is relatively high, then this will place downward pressure on the company’s gross profit. For this reason, companies sometimes choose accounting methods that will produce a lower COGS figure, in an attempt to boost their reported profitability. This article discusses the basics of COGM, including its importance and how it is cost of goods manufactured formula calculated. Joint costs are the costs of both raw materials and conversion that cannot be separated. Joint cost allocation is the process by which joint costs are assigned to particular products produced in a process or department. Beginning work in progress inventory is the value of goods recorded as WIP at the start of the financial year or accounting period.

- Here’s what finished goods inventory is, how to calculate it, and why it’s one of the best types of inventory out there.

- After these values, you can put all numbers in the goods manufacture formula and move the items to the ending finished goods inventory account.

- It also includes all expenses, including direct and indirect costs.

- For example, if you pay an employee $25 per hour to provide a service, the cost is $25 per hour.